Executive Snapshot

China’s bitumen market entered early June 2026 with a firm pricing tone despite uneven downstream demand. Public market references showed the benchmark bitumen price above CNY 4,400 per ton on June 5, while Shanghai futures-related references remained around the low CNY 4,100s in early June. The gap between physical-market sentiment and futures settlement references highlights the importance of monitoring multiple sources rather than relying on a single screen price.

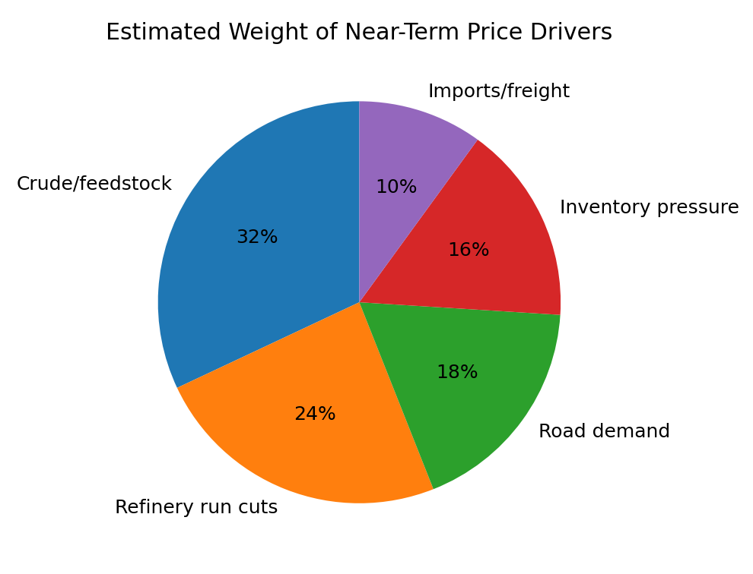

The strongest near-term price support comes from refinery economics and crude availability. Lower crude import flows, reduced refinery throughput, and poor margins have limited the willingness of some producers to run at higher rates. At the same time, road construction demand has been inconsistent because of rainfall, regional project timing, and cautious procurement. The result is a market that is neither strongly bullish nor clearly weak: price levels are supported by supply-side restraint, while buyers remain selective because actual paving demand is not equally strong across all provinces.

Chart 1 - Illustrative China bitumen price movement using public benchmark levels and market-aligned estimates.

1. China Bitumen Price Overview

China bitumen prices in early June 2026 reflected a market supported more by supply discipline than by strong end-user demand. The benchmark level reported by public commodity trackers moved above CNY 4,400 per ton on June 5, indicating that the market had gained momentum from the previous month. This strength did not come from a broad construction boom. Instead, the pricing environment was shaped by constrained refinery operations, lower crude inflows, and cautious producer behavior.

For buyers, the most important point is that China’s bitumen price cannot be read as a single national number. Physical wholesale quotes, futures-linked settlement references, regional truck-delivered offers, and import parity calculations can all show different levels. A procurement team comparing China with Southeast Asian or Middle Eastern alternatives must separate refinery gate pricing from delivered cost.

The market is currently sensitive to marginal changes in refinery runs. If producers lift output aggressively, regional prices could soften quickly. If crude availability remains tight and margins stay weak, supply-side support may continue even when road demand is patchy.

2. Historical Price Movement in 2026

The first half of 2026 has been characterized by gradual price recovery rather than a straight upward rally. Early-year pricing remained relatively cautious as construction activity had not yet reached peak season. By March and April, market references began showing firmer levels as refiners faced narrower margins and buyers started preparing for seasonal road demand.

The June price signal is important because it arrived at a time when China’s wider petroleum market was under pressure from weak gasoline and diesel consumption. In theory, weak fuel demand can reduce refinery appetite and limit feedstock processing, indirectly reducing bitumen availability. That creates a different price pattern from a classic demand-led rally: the price can strengthen even while downstream buying remains selective.

A disciplined reading of 2026 prices should therefore look at three layers: futures settlement levels, wholesale physical surveys, and local delivered quotes. If all three move upward together, the market is genuinely tight. If only one-layer rises, the move may be temporary or driven by local supply conditions.

3. Crude Oil Imports and Bitumen Price Impact

China’s crude import behavior has become one of the most important price drivers for the bitumen market. Reuters reported in early June 2026 that China was drawing more heavily on oil stockpiles as seaborne imports fell to unusually low levels. For bitumen, this matters because reduced crude availability can affect refinery operating decisions and the production balance between fuel products, residual streams, and asphalt-related output.

Bitumen production competes for refinery attention with other products. When refiners face weak margins or limited feedstock flexibility, they may choose to reduce throughput or adjust product slates. That can tighten bitumen supply even if construction demand is not especially strong. This is why upstream crude signals are often watched alongside downstream road activity.

A lower crude import environment does not automatically mean higher bitumen prices, but it raises the probability of supply discipline. If refinery runs remain suppressed, inventories may decline and wholesale offers can become firmer. If crude imports recover and refinery utilization improves, supply pressure may return and cap further price gains.

Table 1 - Crude and refinery signals affecting bitumen price

|

Signal

|

Current reading

|

Bitumen implication

|

|

Lower crude imports

|

Seaborne arrivals reported unusually low in early June

|

Supports supply discipline

|

|

Stockpile drawdown

|

Commercial inventories used more actively

|

Can delay crude import recovery

|

|

Reduced refinery throughput

|

June runs expected to remain subdued

|

Limits output of refined products including bitumen

|

|

Weak fuel demand

|

Gasoline/diesel demand under pressure

|

Can reduce refinery operating appetite

|

4. Refinery Runs and Production Margins

Refinery economics have had a direct influence on China’s bitumen price formation. S&P Global reported that Chinese refineries were likely to extend lower crude throughput into June because of limited feedstock, soft oil-product demand, and elevated inventories. A reduction in refinery runs can reduce the volume of bitumen available to regional distributors, especially when producers are unwilling to sell at levels that do not cover operating economics.

Margins are particularly important for independent refiners. When gasoline and diesel demand weakens, refiners may struggle to justify higher runs. Bitumen then becomes part of a broader optimization decision rather than a standalone market. Producers may slow output, focus on alternative products, or time sales around stronger demand windows.

For traders, refinery behavior is often more useful than headline demand commentary. A weak demand market with falling refinery supply can still hold firm. A stronger demand market with heavy refinery output can remain capped. The balance between these two forces determines whether price gains are sustainable.

5. Regional Price Differences Across China

China’s bitumen market has clear regional differences because road demand, rainfall, refinery access, storage capacity, and coastal import options vary by province. East China often reflects a combination of industrial activity, port accessibility, and stronger trading liquidity. South China can be influenced by imported cargo availability and weather-related construction delays. North China pricing may react more strongly to infrastructure project scheduling and refinery supply shifts.

Regional spreads matter because national averages can hide local tightness. A buyer in Guangdong may face a different procurement environment from a buyer in Shandong or Sichuan. Delivered cost, not just wholesale price, determines the practical market level. Regional logistics constraints can turn a moderate national market into a tight local market.

The most useful approach is to compare regional price indices rather than individual quotes. A sustained premium in one region usually indicates either stronger demand, weaker supply, or higher replacement cost. Temporary deviations often disappear when weather improves or cargoes move between regions.

Chart 2 - Regional price index illustrates how local conditions can diverge from the national midpoint.

6. South China Market Conditions

South China is particularly sensitive to weather, coastal cargo availability, and project execution schedules. Rainfall can delay paving activity and reduce immediate consumption, but it does not necessarily remove demand. Deferred projects may return later, creating a delayed buying wave if contractors need to recover lost work time.

The region also has greater exposure to import competition than inland markets. When imported cargoes are competitively priced, domestic producers may need to adjust offers to protect share. When import economics weaken, local suppliers gain more pricing leverage. This relationship makes South China an important indicator for traders watching import parity.

Market sentiment in South China can shift quickly. A few weeks of weak paving demand may pressure local offers, while refinery constraints or port delays can reverse that softness. Buyers in the region usually benefit from monitoring both domestic producer quotes and imported cargo indications.

7. East China Market Conditions

East China is one of the most liquid zones in the domestic bitumen market. The region combines coastal access, strong industrial demand, dense infrastructure networks, and active trading channels. Price signals from East China often influence wider market sentiment because buyers and sellers treat it as a practical reference point for commercial activity.

Demand in East China is closely linked to urban maintenance, expressway projects, municipal works, and industrial construction. Unlike some regions that depend heavily on seasonal road programs, East China can support more diversified consumption. This does not eliminate volatility, but it makes the region a useful indicator of underlying market strength.

Supply availability is also relatively flexible. Producers, traders, and import channels can all influence local price direction. If East China prices strengthen while inventories remain manageable, the move may reflect genuine demand. If prices rise despite low consumption, supply constraints are more likely responsible.

8. North and Northeast China Market Conditions

North and Northeast China often show stronger seasonality than coastal southern markets. Harsh winter conditions can limit paving activity, while warmer months can trigger concentrated procurement for road maintenance and construction. This seasonal compression means buyers may face short periods of intense demand rather than a smooth consumption curve.

Prices in these regions can be affected by project timing and inventory preparation. Contractors and distributors may build stock ahead of the active season, creating a temporary rise in demand before actual paving peaks. If supply is limited during that window, local prices can move faster than national averages.

The Northeast also tends to be more exposed to logistics and refinery scheduling. When production or delivery timing is disrupted, replacement options may be less flexible than in coastal trading hubs. This can create local premiums even when the national market looks balanced.

9. Inventory Levels and Buyer Sentiment

Inventory is one of the clearest indicators of whether China’s bitumen price has room to move higher. When producer and trader stocks are low, sellers gain confidence and buyers may move quickly to secure supply. When inventories rise, even strong headline prices can become vulnerable to correction.

Buyer sentiment in June 2026 appears selective rather than aggressive. Contractors are not purchasing blindly; they are comparing project schedules, weather conditions, and available credit before committing to larger volumes. This behavior can slow price increases because sellers need actual consumption to confirm market strength.

Inventory interpretation should be regional. High stocks in one province do not necessarily relieve shortages elsewhere. Inland regions may remain tight even when coastal storage looks comfortable. For this reason, a national inventory number should be treated as a starting point, not a complete price signal.

10. Infrastructure Demand and Road Construction

Infrastructure spending remains the long-term backbone of China’s bitumen demand. Road maintenance, expressway expansion, urban resurfacing, port access roads, and industrial logistics corridors all require steady asphalt material supply. However, the timing of government approvals and contractor mobilization can create uneven buying patterns.

The demand side in 2026 is not a simple story of expansion. China’s economy is adjusting to weaker property activity and shifting investment priorities, while high-tech manufacturing and selected infrastructure programs remain supported. This means bitumen demand may perform better in regions with active public works than in areas exposed to weaker private-sector construction.

For price analysis, approved project pipelines are more important than broad construction headlines. A national infrastructure policy can support sentiment, but actual bitumen consumption depends on road projects entering execution. Traders should track tender awards, maintenance budgets, and weather windows to judge real demand.

Table 2 - Demand indicators relevant to China bitumen price

|

Indicator

|

Why it matters

|

Price signal

|

|

Road project execution

|

Actual paving work consumes material

|

Direct demand support

|

|

Rainfall patterns

|

Can delay construction and postpone buying

|

Short-term pressure

|

|

Municipal maintenance budgets

|

Supports recurring demand

|

Stable baseline consumption

|

|

Expressway expansion

|

Creates bulk procurement requirements

|

Medium-term price support

|

11. Import Competition and Replacement Cost

Imported bitumen can act as a pricing ceiling in coastal Chinese markets when replacement cargoes are available at competitive levels. If domestic offers rise too far above import parity, buyers may consider alternative origins. However, import competition depends on freight, currency, cargo availability, delivery timing, and quality specifications.

China’s import dynamics are also influenced by the wider Asian market. When Southeast Asian buyers are active, cargo availability for China may tighten. When regional demand softens, imported material can become more competitive and pressure domestic suppliers. This creates a feedback loop between China, Southeast Asia, and the Middle East.

Replacement cost is the key concept. A buyer does not compare domestic price only with a foreign FOB price; the comparison must include freight, handling, customs, storage, and delivery timing. If the landed import cost remains above local quotes, domestic prices have room to rise before import pressure becomes serious.

12. Export Pricing and Modified Bitumen Products

China is not only a consumer of bitumen; it also participates in export markets, especially through bitumen and modified bitumen products. Sunsirs reported that China exported 236,000 tons of bitumen and modified bitumen products in the first quarter of 2026, up from 211,000 tons in the same period of 2025, with an average export price around US$375 per ton.

Export performance can influence domestic pricing when producers have the option to redirect volume overseas. If export demand improves, domestic availability may tighten, particularly for specific grades or modified products. If overseas demand weakens, more material may remain in the local market and pressure domestic offers.

Modified bitumen exports are especially relevant because they are tied to higher-value applications and project specifications. A stronger export pull for specialty products can improve refinery and blending margins even if ordinary paving-grade demand is moderate.

Table 3 - China bitumen export context

|

Metric

|

Q1 2026 reading

|

Market interpretation

|

|

Bitumen and modified bitumen exports

|

236,000 tonnes

|

Higher export pull than Q1 2025

|

|

Year-on-year change

|

+11.8%

|

Overseas demand improved

|

|

Average export price

|

US$375/t

|

Stable export pricing environment

|

|

February effect

|

Temporary dip during Spring Festival

|

Seasonal disruption, not structural weakness

|

13. Government Fuel Pricing and Refinery Behavior

China’s regulated fuel pricing system affects bitumen indirectly by shaping refinery incentives. Reuters reported that China planned to reduce domestic gasoline and diesel ceiling prices from June 5, 2026, after earlier increases linked to global energy market volatility. For refiners, capped or adjusted fuel prices influence overall product margins and can affect decisions about crude throughput.

When refiners face losses in major fuel products, they may reduce runs or change product allocation. Bitumen supply can tighten as a secondary consequence. The market therefore needs to watch fuel price adjustments even when bitumen itself is not directly regulated in the same way.

This indirect policy channel is important for commercial planning. A procurement team focused only on road demand may miss a supply-side shift caused by fuel-price policy and refinery economics. In China, bitumen price analysis must combine construction demand with energy policy signals.

Chart 4 - Lower refinery throughput can be associated with firmer bitumen pricing when supply tightens.

14. Price Forecast for Q3-Q4 2026

The base-case outlook for China bitumen prices points to range-bound firmness rather than a one-way rally. Supply constraints, reduced refinery runs, and crude availability support the market, while uneven paving demand and cautious purchasing limit upside. If construction activity improves after weather disruptions, prices may hold above early-year averages through Q3.

A bullish scenario would require three conditions: refinery supply remains constrained, road demand accelerates, and import replacement costs stay high. Under that combination, regional premiums could widen and physical prices may continue moving upward. A bearish scenario would emerge if refinery output recovers quickly while demand remains delayed or inventories rise.

For Q4, seasonal demand typically weakens in colder regions, but policy-driven road spending can soften the decline. The market is likely to remain highly regional. East and South China may respond differently from North and Northeast China depending on project completion schedules and stock levels.

Table 4 - China bitumen price scenario matrix for 2026

|

Scenario

|

Conditions

|

Likely price behavior

|

|

Tight supply case

|

Low refinery runs, stronger road demand, high replacement cost

|

Prices move higher or hold firm

|

|

Base case

|

Balanced demand, selective buying, limited supply recovery

|

Prices remain range-bound

|

|

Soft demand case

|

Weak construction, inventory build, easier crude availability

|

Prices retreat toward lower range

|

Chart 5 - Scenario view for China bitumen prices through Q4 2026.

15. Buyer Strategy and Market Monitoring

Buyers should avoid treating China’s bitumen market as a single-price environment. The most effective procurement strategy compares futures references, physical wholesale surveys, refinery operating conditions, regional inventory levels, and import replacement cost. A quote that appears expensive on a national basis may be competitive in a tight local region.

Contract timing is equally important. During periods of uncertain demand, spot buying can preserve flexibility. During periods of refinery constraint, short-term purchasing may expose buyers to sudden availability risk. Large contractors and distributors may benefit from a blended approach: secure base supply through agreed volumes while leaving part of demand open for market opportunities.

Source Links

Bitumen Magazine: http://www.bitumenmag.com/

Trading Economics - Bitumen price chart: https://tradingeconomics.com/commodity/bitumen

Mysteel - China heavy-traffic bitumen wholesale prices, June 2, 2026: https://www.mysteel.net/news/5126388-flash-china-heavy-traffic-bitumen-wholesale-prices-20260602

CEIC - Shanghai Futures Exchange petroleum bitumen settlement reference: https://www.ceicdata.com/en/china/shanghai-futures-exchange-commodity-futures-settlement-price-daily/cn-settlement-price-shanghai-future-exchange-petroleum-bitumen-6th-month

SHFE - Bitumen futures contract information: https://www.shfe.com.cn/eng/Market/Futures/Energy/bu_f/

Reuters - China oil stockpiles and crude imports, June 2, 2026: https://www.reuters.com/business/energy/china-seen-tapping-deeper-into-oil-stockpiles-imports-hit-decade-low-2026-06-02/

Reuters - China gasoline and diesel price cut, June 5, 2026: https://www.reuters.com/world/asia-pacific/china-cut-domestic-retail-gasoline-diesel-prices-june-5-2026-06-04/

S&P Global - China refinery runs and supply conditions: https://www.spglobal.com/energy/en/news-research/latest-news/shipping/052926-china-may-extend-refining-run-cuts-in-june-amid-tight-supply-low-demand

Sunsirs - China asphalt/bitumen market and export data, May 2026: https://www.sunsirs.com/commodity-news/petail-32843.html

Baiinfo - China heavy traffic bitumen price reference: https://en.baiinfo.com/products/5/0/0?channel=90